The 288,000 gain in employment in the U.S. was the biggest since January 2012 and followed a revised 203,000 increase the prior month that was stronger than initially estimated, Labor Department figures showed today. The median forecast in a Bloomberg survey of economists called for a 218,000 advance. Unemployment dropped from 6.7 percent to the lowest level since September 2008 as fewer people entered the labor force. Wages and hours worked were stagnant. More concerning, participation levels declined dramatically.

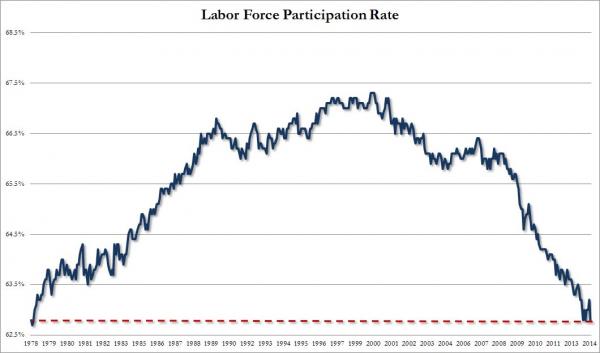

Once again, we are reminded of statistical biases in Labor Market Statistics in the U.S., as provided by the Department of Labour (sorry, Labor). While the Establishment Survey job number was a whopper, and the biggest monthly addition since January 2012, the Household Survey showed an actual decline of 73,000 jobs. What is much worse, is that the reason the unemployment rate tumbled is well-known: it was mainly due to the number of NON WORKING Americans dropping out of the labor force (i.e. the numerator and denominator of the statistic decrease in same absolutes). The labor force participation rate crashed from 63.2% to 62.8%, the lowest since January 1978.

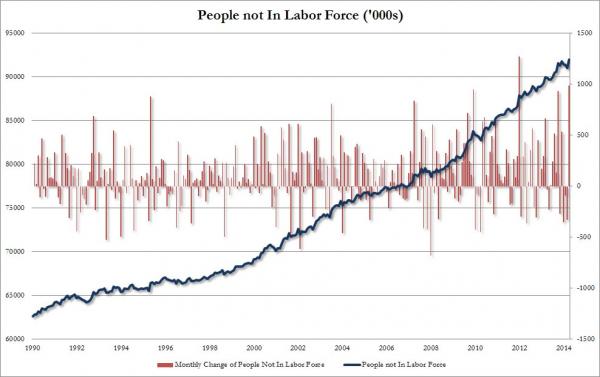

Stated in another way, the number of people not in the labor force soared to 92 million, the second highest monthly increase ever, or only 988,000 ‘better’ than January 2012 which curiously was the one month when the establishment survey reported a 360,000 “increase” in jobs.

Zero Hedge puts the end result in great perspective: “the number of people out of the labor force is now an all time high 92 million, and the labor force tumbled by 800,000 to 155.4 million from 156.2 million, as the delayed effect of the extended jobless benefits ending finally hit the stats. What is most amusing is that the “persons who currently want a job” was unchanged at 6,146,000 – even the BLS said it was “puzzled why so many unemployed people are not looking for jobs.” We have some ideas, and no, they don’t include the addition of only 234,000 “birth/death adjustment” jobs.

U.S. Labour (sorry, Labor) Participation Rate:

People not in the labor force: